Aries Newsletter – Volume 1, Issue 1

February 2016 P&I Renewal

The recently concluded renewal was one of the most difficult renewals that has been experienced in many years. The majority of shipping companies faced unbelievably bad trading conditions, and the Clubs, with average general increase under 2% had comparatively little wiggle room with regards to their premium requirements. However, some owners with very good or improved loss records managed decent reductions in an overall “soft” market.

Some respite was afforded owners by a reduction in the cost of the group reinsurance programme which was passed on to members, but this has come at a potential cost as the individual club retentions have risen to $ 10 million and Hydra is assuming a bigger share of the higher levels of risk.

We herein provide a table that shows the International Group Excess Reinsurance Rates for 2016/17 and comparison against 2015 (see page 2). We also enclose the Group circular detailing the changes to the structure of the worlds largest reinsurance contract.

Perhaps as a result of the circumstances outlined above, the renewal itself was something of a slow burner, which only really came to life in the last 10 days or so. Unlike in previous years, there were no clear winners or losers, although the big move by Gard into the cruise ship industry was notable.

Having secured a 25% share of Carnival (along with the UK Club, from Standard) in a move fixed late last year, they also added a significant number of RCCL vessels.

Only two clubs have issued official reports on their renewals. Gard achieved a 2.8million GT increase, making 10.7million GT increase on the year – this represents a 5% increase in owned GT. The growth is made up of both new business and increased GT on existing business. Skuld’s year on year growth was 9million GT (a greater percentage growth than Gard) with much of the growth being in the offshore sector, with more modest increases in the bluewater P&I arena.

The impact of the renewal was almost immediately overshadowed by confirmation of the strong rumour that Britannia and the UK Club were about to enter into merger discussions. These negotiations are now well under way, as are discussions to merge their respective management companies, and it is expected that the matter will be put to their respective members at Special General Meetings later in the year. No further details have emerged as to how such a merger could be accomplished.

Group Excess Reinsurance Rates 2016/17

The International Group RI rates (per GT) including Hydra premium, Collective Overspill Cover and Excess war risk P&I for the year commencing 20 February 2016 are as follows:

|

2015/16 |

2016/17 |

Adj in ETC |

%AGE CHANGE |

||

| Tanker Dirty |

0.7317 | 0.6567 | -0.075 | -10.25% | |

| Tanker Clean | 0.3138 | 0.2816 | -0.0322 | -10.26% | |

| Dry | 0.4888 | 0.4537 | -0.0351 | -7.18% | |

| Passenger | 3.7791 | 3.5073 | -0.2718 | -7.19% |

Chartered Entries

Reinsurance Costs including excess war risks will be $0.2380 (2015 $0.2522) for chartered tankers, and $0.1163 (2015 $0.1228) for chartered dries.

US Oil Pollution Surcharge 2016/17

Following the decision taken for the last two policy years, the surcharge will remain at nil for 2016/17.

International Group reinsurance renewal update January 2016

(source: http://www.igpandi.org/News+and+Information/News/2016/294)

The arrangements for the renewal of the International Group General Excess of Loss reinsurance contract and the Hydra reinsurance programmes for 2016/17 have now been finalized.

The individual club retention will increase with effect from 20 February 2016 to US $10 million, and the attachment point on the GXL contract will remain unchanged, at US $80 million, for the 2016/17 policy year.

The loss experience of the reinsurance programme on the 2012/13, 2013/14, 2014/15 and 2015/16 (year to date) remains favourable to reinsurers, with currently only one claim notified to the GXL for 2015/16. This, combined with increased market capacity, the continuing positive financial development of the Group captive, Hydra, facilitating additional Hydra risk retention, and the use of a third multi-year fixed placement, has enabled the Group to achieve advantageous reinsurance renewal terms, with reductions across all layers of the programme and on the Excess War P&I cover, resulting in reinsurance rate reductions across all vessel categories.

In addition to the two 5% 36 month private placements of US $1 billion xs US $100 million which incepted on the 2014/15 and 2015/16 renewals respectively, a third 5% 36 month private placement of US $1 billion excess US$100 million will incept from 20 February 2016.

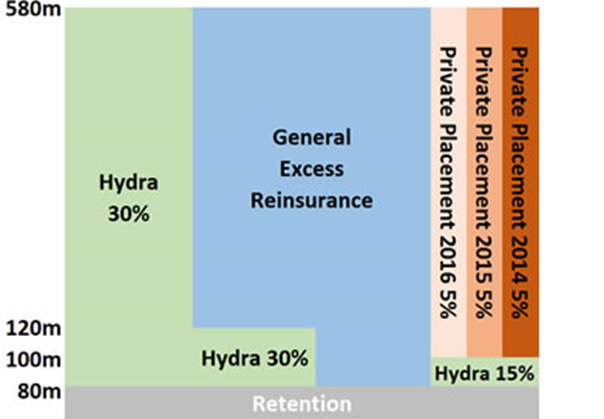

Hydra reinsurance of the Group pool will remain unchanged at US $50m xs US$30m. Hydra’s coinsurance share in the first layer of the Group GXL programme (US $500 million xs US $80 million) will increase slightly for 2016/17 to include a further 5% share of the layer US $80 million-US $100 million.

In addition, the scope of the reinsurance cover will be extended from 20 February 2016 to include Nuclear Risks liabilities arising under approved certificates, guarantees or undertakings, up to a limit of US $1 billion.

The diagram below illustrates the revised participation structure of the first layer of the Group GXL programme for 2016/17.

IG GXL Layer 1 structure 2016/17

For 2016/17 there will be a new simplified two layer pool structure, with a lower pool layer from US$ 10 million to US$45 million. The current upper, and upper-upper, pool layers will be replaced by a single upper pool layer from US $45 million to US $80 million, with a claiming club retention rate of 7.5% across the combined layer.

In approaching the reinsurance cost allocation exercise for the 2016/17 policy year, and in accordance with the Group’s general allocation objective, principally that of moving towards a claims versus premium balance for each vessel type over the medium to longer term, the Group’s Reinsurance Strategy Working Group and Reinsurance Subcommittee have again reviewed the updated historical loss versus premium records of the current four vessel type categories.

In the tanker category, the 2015 “Alpine Eternity” incident brought to an end a run of five years of reducing claims, although tanker claims still only account for just over 10% of overall claims.

In the dry cargo category, during 2015/16 claims and premium have continued to move closer to equilibrium. In comparing container and non-container dry tonnage, the objective stated above of seeking to achieve equilibrium over the medium to longer term, does not justify the creation of a new vessel type category should not be created in the short term, absent a compelling reason to do so based on a sustained claims pattern.

The absence of any significant container claims arising during the 2015/16 policy year to date means that there remains insufficient historical claims data to support separate treatment of container vessels from dry cargo vessels for reinsurance cost rating purposes for the 2016/17 policy year.

In the passenger category, there were significant increases in reinsurance costs allocated in the 2013/14 and 2014/15 policy years, principally reflecting the very substantial continuing adverse development during those years on claims arising from the Costa Concordia incident. There is unlikely to be any further significant development on these claims, and, in the absence of any further major passenger vessel incidents, the sector should continue to move towards claims/premium equilibrium over the medium term.

The result of the renewal negotiations and programme restructuring is a reduction in reinsurance cost of approximately 10.2% for clean and dirty tankers, and approximately 7.2 % for dry cargo vessels and passenger vessels. Chartered rates are reduced by approximately 5.6% for chartered tankers, and 5.3% for chartered dries.

2016/17 rates summary

| Tonnage Category | 2016 rate per gt | % change from 2015 | |

| DIRTY TANKERS | $0.6567 | % – 10.25 | |

| CLEAN TANKERS | $0.2816 | % – 10.26 | |

| DRY CARGO VESSELS | $0.4537 | % – 7.18 | |

| PASSENGER VESSELS | $3.5073 | % – 7.19 | |

| CHART TANKERS | $0.2380 | % – 5.63 | |

| CHART DRIES | $0.1163 | % – 5.29 |

Paul Jennings

Chairman, International Group Reinsurance subcommittee